Ai For Nbfcs And Banks In India: A Practical Guide

- 10 min read

India’s financial services sector has built more credit infrastructure in the last decade than many countries have built in three.

Aadhaar. UPI. Digital KYC. The Account Aggregator framework. Digital Lending guidelines. Co-lending. Default Loss Guarantee rules. ULI. The DPDP Act. Scale-Based Regulation for NBFCs.

Each of these has reshaped how banks and NBFCs operate. What feels routine today would have been difficult to imagine a decade ago.

The result is a credit ecosystem with public rails that few large markets can match.

Customers are reachable. Data can be shared with consent. Disbursement can happen in real time. Compliance boundaries are clearer. Regulated entities are more deliberately defined.

AI is what unlocks the next layer of value on top of this infrastructure.

But it also creates new risks if applied without discipline.

RBI has been clear: automation does not remove supervisory responsibility. Outsourced models do not transfer accountability. Digital lending guidelines apply whether the lender is a bank, an NBFC, or part of a partnership model. Customer protection is non-negotiable. Model risk is a board-level concern.

This guide explains what AI for NBFCs and banks in India really involves, where it creates value, what makes the architecture different from generic banking AI, and how institutions can build AI that respects both regulation and ground-level operating reality.

Why AI for Indian NBFCs and Banks Is a Different Conversation

Banking AI may be a global category, but AI for Indian NBFCs and banks is a much more specific discussion.

The Regulatory Frame Is Specific

AI in Indian financial services must operate inside a detailed and evolving regulatory environment.

This includes:

- Scale-Based Regulation for NBFCs

- Digital Lending directions

- KYC and AML rules

- Outsourcing of Financial Services framework

- Fraud Risk Management directions

- DPDP Act requirements for financial data

- IT framework expectations for NBFCs

This is not a loose environment. It is supervised, detailed, and continuously evolving.

The Product Mix Is Specific

NBFCs are not simply smaller banks.

They often focus on specific product categories such as:

- Vehicle finance

- Gold loans

- Microfinance

- Housing finance

- MSME credit

- Consumer durable loans

Each category has different customers, data signals, underwriting questions, repayment behavior, and collections realities.

AI models designed for universal banking cannot be copied blindly into NBFC workflows.

The Customer Base Is Highly Diverse

Indian financial services serves customers across income levels, geographies, languages, devices, and digital comfort levels.

AI built only for urban, English-speaking, digitally fluent customers will fail a large part of the market.

AI for Indian banks and NBFCs must work for real customers in real conditions. That means vernacular support, low-connectivity tolerance, assisted journeys, voice interfaces, trust-building design, and simple escalation paths matter deeply.

Co-Lending and Partnership Models Are Central

Banks and NBFCs often work together.

NBFCs may originate. Banks may fund. Loan service providers may source. Lenders may disburse. Servicing may involve multiple parties.

AI has to support this operating reality with clear accountability, reporting, customer handling, and regulatory ownership.

India Has Public Credit Infrastructure Other Markets Do Not

India Stack, UPI, Aadhaar, Account Aggregator, and ULI are not concepts. They are working infrastructure.

AI systems that ignore these rails create unnecessary friction. AI systems that use them intelligently can move faster, improve data quality, reduce cost, and strengthen consent-based workflows.

These five factors define the design space.

AI built with them in mind can scale. AI built without them often underperforms or runs into regulatory friction.

Where AI Creates Real Value for NBFCs and Banks in India

AI creates the most value where workflows are high-volume, decisions are repeatable, and institutions need speed without weakening compliance or customer outcomes.

Digital Lending: From Origination to Disbursement

Digital lending is one of the clearest areas where AI can create visible impact.

AI can support:

- Application intake

- KYC workflows

- Underwriting decision support

- Risk-based pricing

- Document processing

- Disbursement orchestration

- Post-disbursement communication

Because RBI has clearly defined expectations for digital lending, this is also one of the areas where AI must be built with strong governance from the beginning.

Underwriting Thin-File and New-to-Credit Customers

Many Indian borrowers do not have deep bureau histories.

AI can help combine bureau data, Account Aggregator data, bank statements, GST information, payroll data where available, transaction signals, and contextual data to support safer underwriting.

This is especially important for new-to-credit and thin-file lending.

When designed properly, AI can help institutions lend beyond traditional bureau scores without losing risk discipline.

Collections and Customer Financial Assistance

Collections is one of the most operationally painful areas for many NBFCs.

AI can help with:

- Account segmentation

- Cure-path prediction

- Channel and timing optimization

- Regional-language outreach

- Settlement and restructuring support

- Customer assistance workflows

The key is discipline.

Collections AI must improve efficiency without weakening conduct standards or customer protection.

Fraud, AML, and Synthetic Identity

India’s transaction volumes are high, and fraud patterns are increasingly sophisticated.

AI can support detection of:

- Application fraud

- Mule accounts

- Agent and channel fraud

- Synthetic identities

- AML transaction anomalies

But explainability matters. Investigations must be defensible, auditable, and understandable to internal teams and supervisors.

Customer Service and Vernacular Conversational AI

AI-powered service across Hindi, Tamil, Telugu, Bengali, Marathi, Gujarati, Kannada, Malayalam, and English can significantly improve customer support.

Voice and text AI can support:

- Service queries

- Transaction queries

- EMI questions

- Complaint handling

- Status updates

- Assisted journeys

The strongest systems are not just multilingual. They are escalation-aware, compliance-aware, and designed for real customer behavior.

Co-Lending and Partnership Operations

Co-lending creates coordination complexity.

AI can help with:

- Reconciling shared books

- Routing customer interactions to the correct entity

- Maintaining the regulatory split

- Supporting reporting on both sides

- Reducing repetitive operational coordination

This may not always be the most visible AI use case, but it can create meaningful productivity gains.

Compliance and Regulatory Reporting

AI does not replace compliance teams.

It gives them leverage.

AI can assist with return preparation, sample reviews, exception investigations, audit trail assembly, policy checks, and documentation support.

In high-volume environments, this can make compliance workflows faster, more consistent, and easier to review.

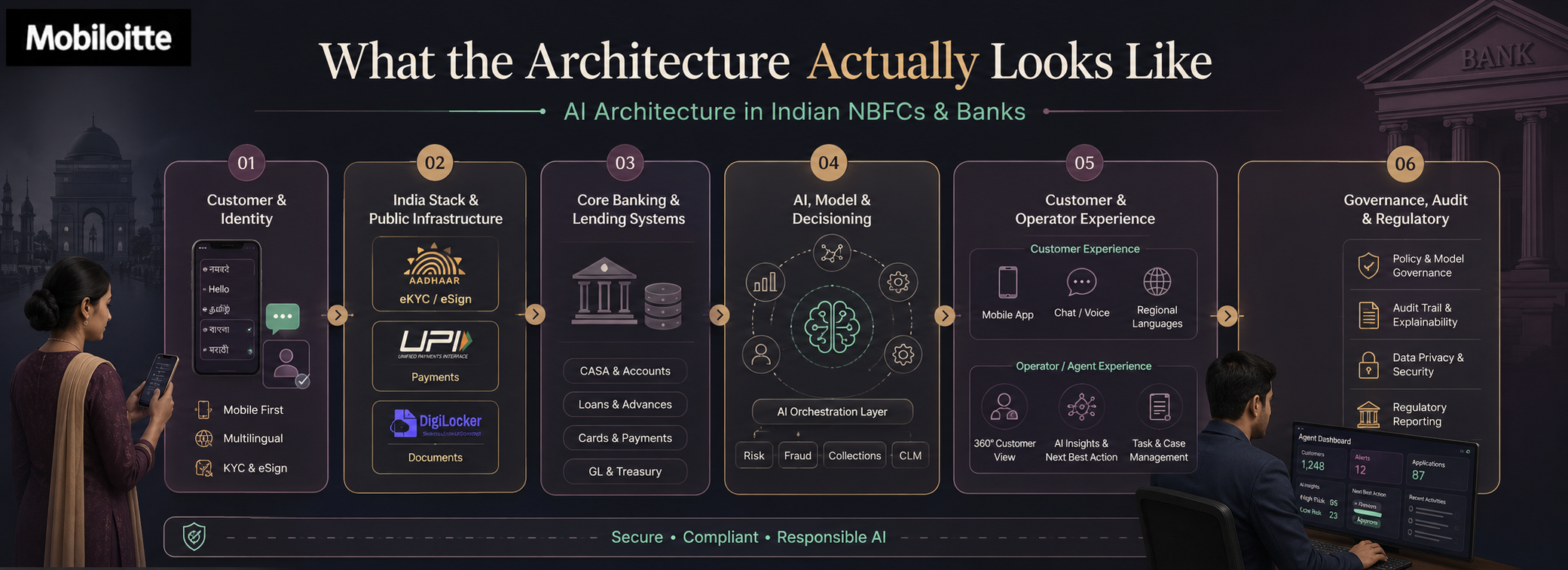

What the Architecture Actually Looks Like

Strong AI architecture for Indian NBFCs and banks shares some components with global banking AI, but it also needs layers specific to India’s regulatory and infrastructure context.

Six layers matter most.

1. Customer and Identity Layer

This includes Aadhaar-based identity, e-KYC, V-CIP, customer master data, consent registry, and DPDP-aligned data handling.

This layer is foundational because every downstream AI workflow depends on reliable identity and compliant data handling.

2. India Stack and Public Infrastructure Layer

This includes Account Aggregator, UPI, ULI where applicable, credit bureau integrations, GST data, and other public rails.

AI systems that use this layer well can make faster and better-informed decisions.

3. Core Banking and Lending Systems Layer

This includes CBS, LMS, LOS, collections platforms, fraud systems, AML tools, product engines, and policy engines.

AI should connect through governed interfaces, not ad hoc exports created separately for every pilot.

4. AI, Model, and Decisioning Layer

This includes foundation models, traditional ML models, conversational AI, document AI, decision engines, and orchestration.

Model risk management must be built into this layer from the beginning.

5. Customer and Operator Experience Layer

AI must reach both customers and internal users effectively.

This includes mobile apps, conversational channels, agent-assisted workflows, partner portals, underwriter interfaces, collector tools, fraud investigation screens, compliance workflows, and service dashboards.

The design must reflect India’s language, device, network, and trust realities.

6. Governance, Audit, and Regulatory Layer

This includes model inventory, validation, change management, explainability, audit trails, regulatory reporting, incident management, and supervisory readiness.

This layer cannot be added later. It must be part of the architecture from day one.

Common Failure Patterns to Avoid

AI programs in Indian NBFCs and banks often start with good intent but fail to scale because of avoidable mistakes.

Common failure patterns include:

- Building AI without grounding it in RBI-specific directions

- Blurring accountability through vendor or outsourcing arrangements

- Adding AI to digital lending journeys without aligning disclosures, cooling-off rules, and disbursement requirements

- Treating Account Aggregator integration as a pilot feature instead of a lifecycle capability

- Designing collections AI for efficiency without conduct guardrails

- Building underwriting models that work on development data but fail in real customer segments

- Creating AI outputs that underwriters, customers, or supervisors cannot interpret

- Running AI as a technology project instead of a regulated business capability

- Engaging model risk teams too late

None of these failures are inevitable.

But they are only prevented through deliberate design.

How Mobiloitte Approaches AI for Indian NBFCs and Banks

Mobiloitte engineers AI for NBFCs and banks as regulated, integrated, operated software.

The work is built around the specific workflow the AI is meant to support, integrated with core systems and India Stack, governed within RBI’s framework, and designed for the customers and operators who will actually use it.

The process starts with workflow and regulatory analysis together.

Architecture is designed across the six layers from the beginning. Account Aggregator and India Stack are used where they create value. Co-lending and partnership operations are treated as first-class concerns where relevant. Customer protection and conduct considerations are built in early, not added later.

The work usually combines four elements.

Workflow and Regulatory Analysis

This includes understanding the customer journey, operational workflow, applicable directions, and the points where AI takes consequential decisions versus where humans must remain involved.

Architecture

This includes selecting models, integration patterns, decisioning approaches, explainability mechanisms, and operating models that can scale beyond one product or channel.

Engineering

This includes building the AI, integrations, customer-facing surfaces, operator interfaces, model risk infrastructure, and regulatory documentation.

Operating Model

This includes model risk governance, change management, monitoring, incident response, and the improvement cadence needed to operate AI under supervisory expectations.

The result is not an AI pilot.

It is AI that an institution can run as a regulated capability across products, channels, and partnerships.

Conclusion

AI for NBFCs and banks in India is not just about automation.

It is about building regulated intelligence into high-volume financial workflows without weakening trust, accountability, or customer protection.

The opportunity is significant because India already has the rails: identity, payments, consented data, lending infrastructure, and regulatory clarity.

But the institutions that succeed will not be the ones that simply add AI to existing journeys.

They will be the ones that design AI around India’s regulatory frame, customer diversity, public infrastructure, and operational realities.

That is what turns AI from a pilot into a real financial services capability.

FAQs

1.What is AI for NBFCs and banks in India in simple terms?

It is the use of AI in workflows such as digital lending, underwriting, collections, fraud detection, customer service, co-lending, and compliance, built within RBI’s regulatory framework and India’s public credit infrastructure.

2.How is AI for Indian NBFCs and banks different from global banking AI?

India’s AI context is different because of RBI-specific regulations, NBFC product diversity, multilingual customer needs, co-lending models, and public infrastructure such as Aadhaar, UPI, Account Aggregator, and ULI.

3.Does the Digital Lending Master Direction apply to AI in lending?

It applies to digital lending journeys conducted by regulated entities, including through loan service providers. AI used in sourcing, KYC, underwriting, disbursement, servicing, or collections must operate within that framework.

4.What is the role of Account Aggregator in AI underwriting?

Account Aggregator enables consent-based sharing of financial information. AI underwriting can use this structured, customer-consented data to make faster and better-informed decisions.

5.How does AI fit with model risk management?

AI should be part of the model inventory and subject to validation, monitoring, change management, and audit discipline. Existing model risk functions should be extended for AI, not replaced.

6.What is the most common reason AI projects under-deliver in NBFCs and banks?

They often under-deliver when AI is treated as a tech project instead of a regulated business capability, or when RBI requirements, customer diversity, and operational realities are considered too late.